EVMS Has Changed!!! Understanding the Transition from 32 to 27 Guidelines in EIA-748 Revision E

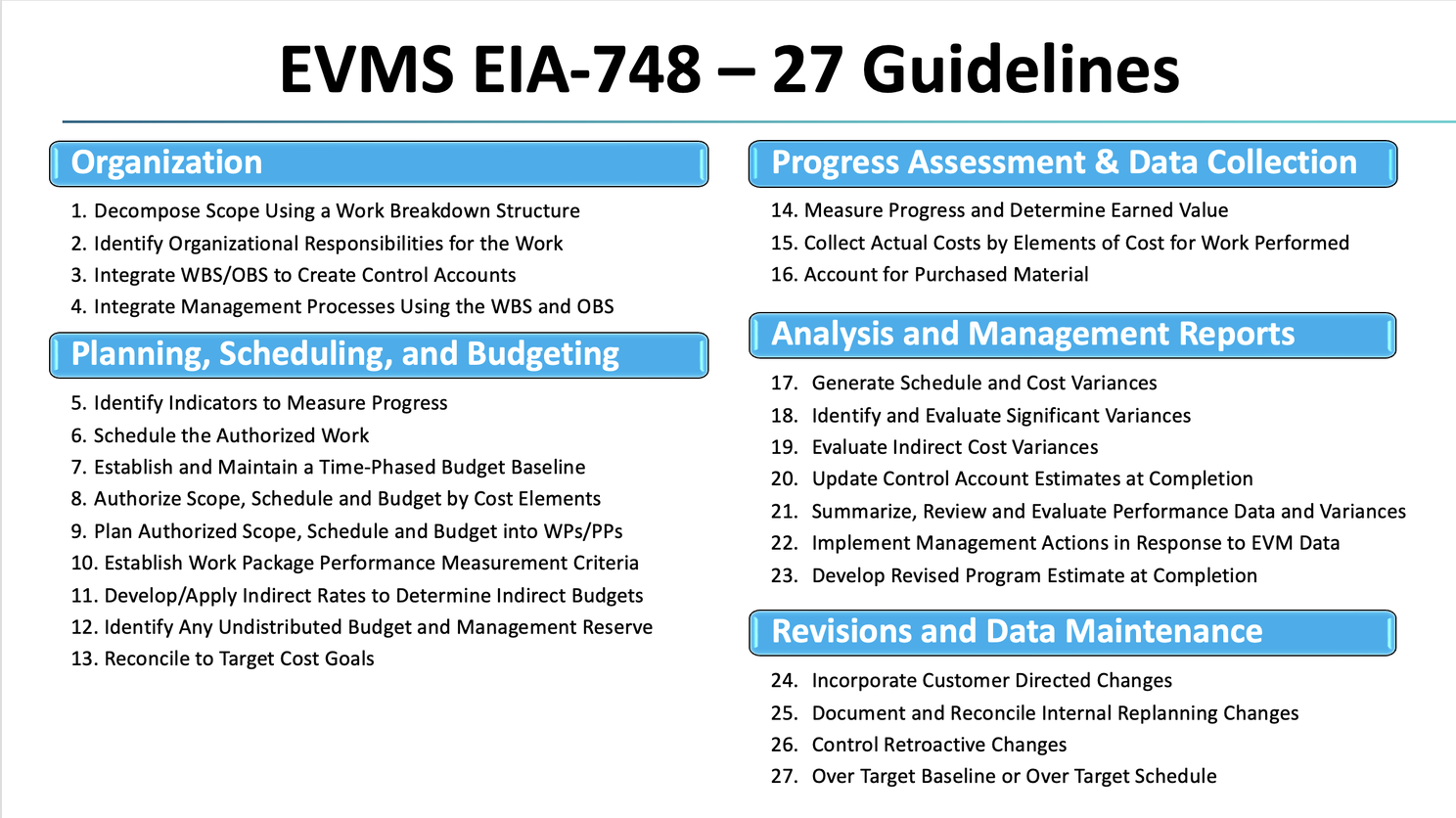

EVMS EIA-748 - 27 Guidelines

On February 16, 2026, SAE International formally released Revision E of the EIA-748 Earned Value Management System standard, marking the first structural evolution of the EVMS framework in decades.

While the foundational principles of Earned Value Management remain intact, the framework governing how organizations implement, demonstrate, and sustain EVMS has been streamlined and clarified.

This is not a cosmetic update. It represents a deliberate modernization of how program performance discipline is structured across complex programs.

For organizations executing cost-type or high-risk programs, the implications are both strategic and operational.

From 32 Guidelines to 27: Streamlining Without Reducing Discipline

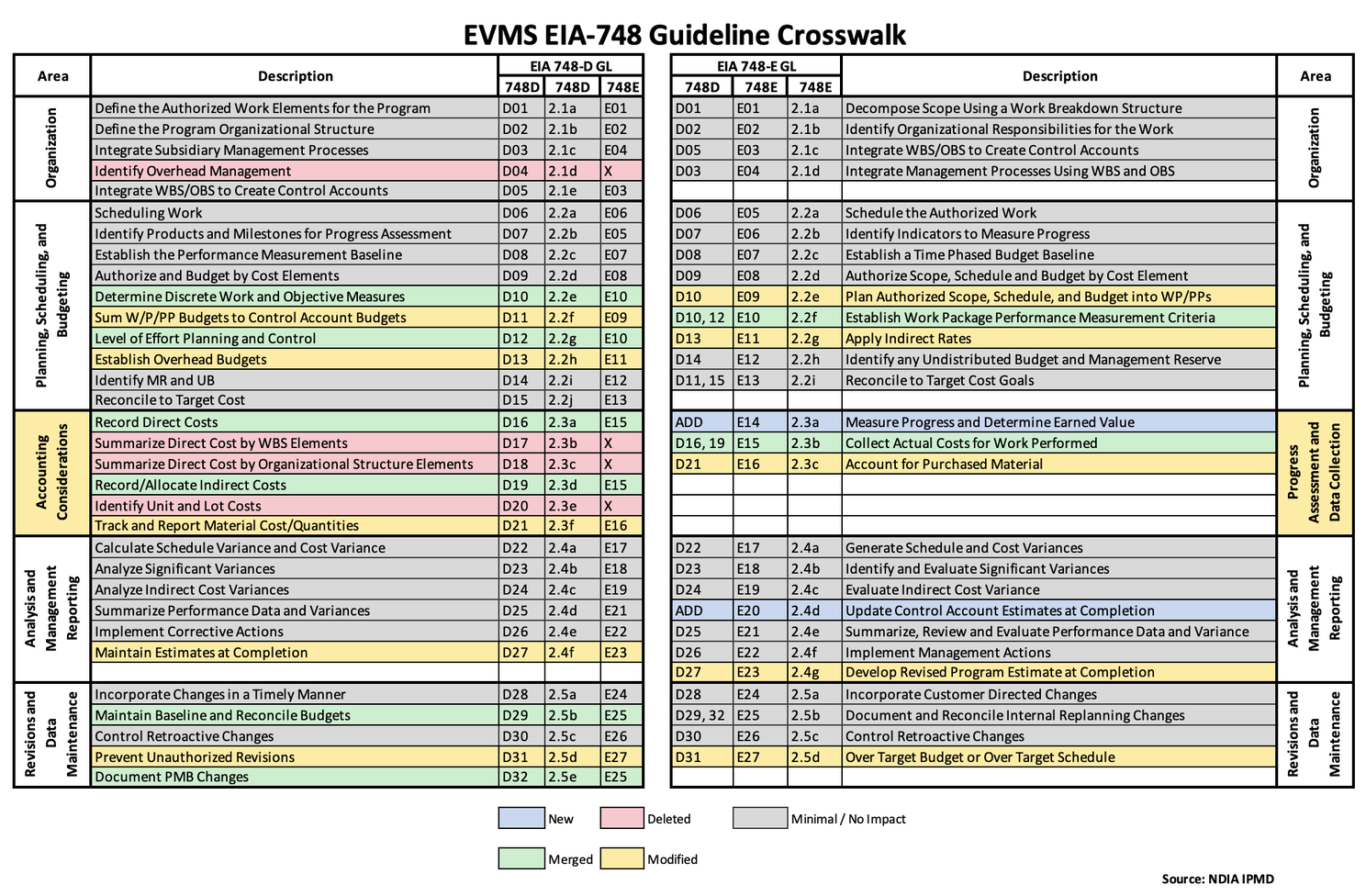

The most visible change is the consolidation of the EVMS guidelines from 32 to 27.

This was not intended to reduce rigor. Rather, the objective was to:

Eliminate redundancy in legacy guidance

Clarify intent for consistent interpretation

Align EVMS with contemporary program execution environments

Emphasize integrated performance measurement

Several legacy guidelines were merged or reframed where modern business systems already provide the necessary management control capability.

The result is a more cohesive and lifecycle-aligned framework.

EVMS EIA-748 Guideline Crosswalk

A Fundamental Philosophical Shift: From Accounting to Performance Measurement

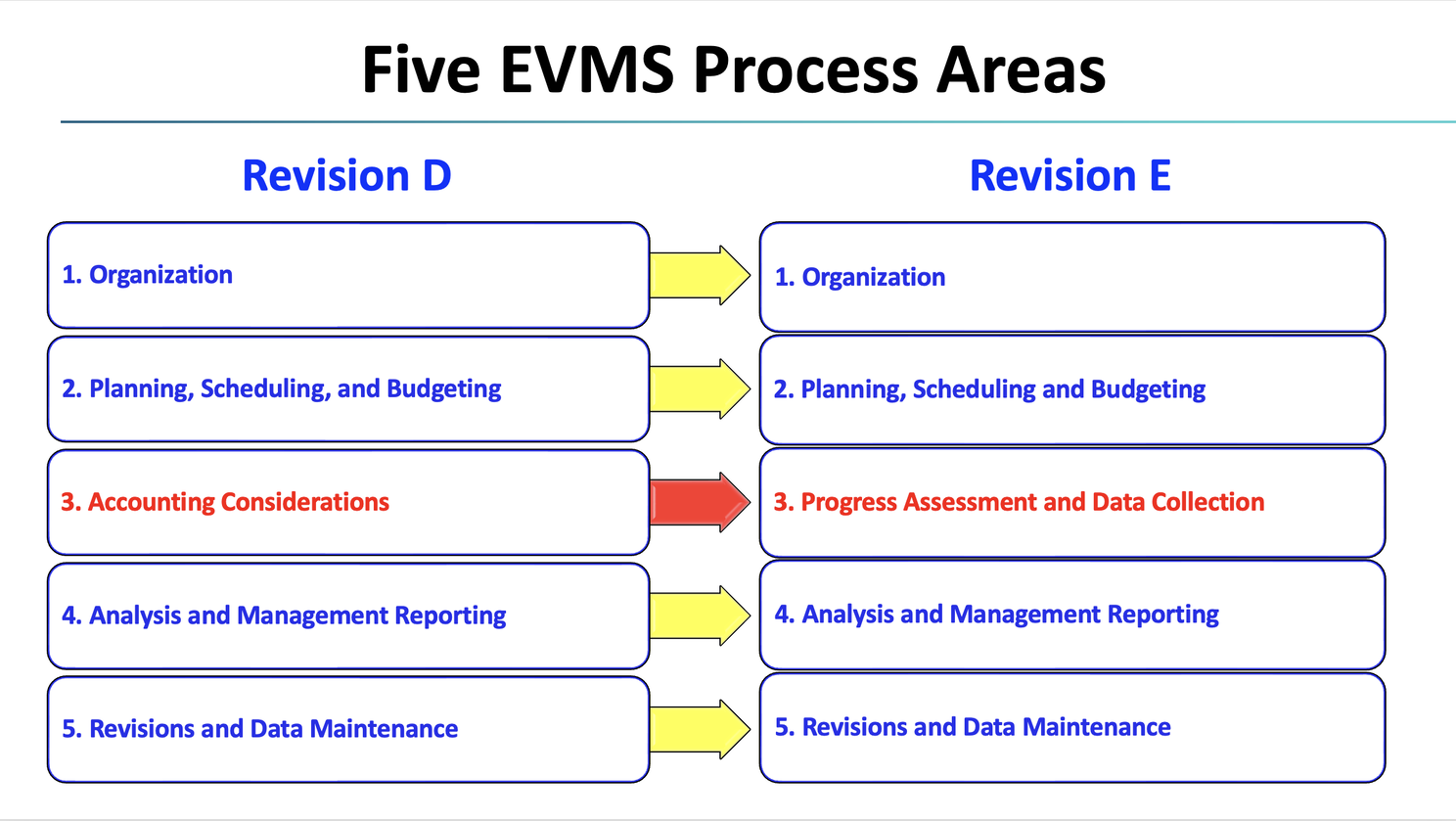

One of the most significant structural changes is the evolution of Process Area 3.

Historically defined as Accounting Considerations, this area is now defined as:

Progress Assessment and Data Collection

This change reflects an important shift in emphasis.

EVMS is being reinforced as a performance management discipline, not an accounting compliance construct.

In practical terms, this means:

Greater focus on objective progress measurement

Stronger integration of cost, schedule, and technical performance

Increased emphasis on forecasting credibility

Enhanced linkage between variance insight and management action

Organizations that historically approached EVMS primarily through cost accumulation processes will need to ensure their systems demonstrate robust performance measurement maturity.

Five EVMS Process Areas

Planning and Baseline Discipline: More Explicit, Not More Burdensome

Revision E strengthens clarity around:

Work authorization logic

Time-phased budget integrity

Performance measurement criteria at the work package level

Indirect rate planning recognition

Management Reserve and Undistributed Budget governance

These elements were always inherent to disciplined EVMS implementations. Revision E simply makes them more structurally explicit.

For mature organizations, this represents validation. For developing systems, it represents a roadmap.

Forecasting and Management Action: Elevated Expectations

Another key refinement is the clearer positioning of forecasting within the management control framework.

Revision E emphasizes:

Control Account level performance forecasting

Program-level Estimate-at-Completion credibility

Management responsiveness to performance signals

Forecasting is no longer viewed as a downstream analytical exercise. It is reinforced as a central component of program execution governance.

This aligns EVMS more directly with executive decision-making.

EVMS EIA-748 - 27 Guidelines

What This Means for Contractors and Program Leadership

Organizations should view Revision E as an opportunity to strengthen program control maturity.

Key considerations include:

Alignment of EVMS Descriptions with revised guideline structure

Reinforcement of objective progress measurement methodologies

Review of forecasting governance practices

Modernization of EVMS training and internal oversight models

Preparation for evolving surveillance interpretation

Importantly, this transition does not invalidate previously accepted EVMS implementations. However, it does reshape the expectations under which performance credibility will be evaluated going forward.

The Strategic Opportunity in Structural Evolution

Periods of standards evolution often create differentiation among organizations.

Those that proactively align tend to achieve:

Stronger performance transparency

Improved forecast realism

Reduced friction during external reviews

Greater executive confidence in program data

Those that delay alignment frequently encounter:

Interpretation challenges

Documentation misalignment

Reactive management behavior

Increased scrutiny during surveillance

Revision E represents a maturation step in the evolution of Earned Value Management.

It reinforces what EVMS was always intended to be:

A management system designed to enable informed decisions, not merely a reporting mechanism.

Final Perspective

The transition from 32 to 27 guidelines reflects a structural refinement, not a philosophical departure.

EVMS discipline remains unchanged. The clarity of expectation has improved. The emphasis on performance credibility has sharpened.

Organizations that recognize both the structural and conceptual implications of Revision E will be better positioned to lead in increasingly complex program environments.

Need Help Navigating EIA-748 Revision E Realignment?

Whether your organization is assessing impacts, updating EVMS documentation, or preparing for future EVMS validation/certification or surveillance expectations, now is the time to ensure your system reflects the refined structure and performance emphasis of the 27-guideline framework.

Elixir Value Management Systems supports organizations across the full EVMS lifecycle:

EVMS implementation, maturity, and compliance

Adoption of EIA-748 Rev E (27-Guideline EVMS framework)

Cost-schedule integration

Project Controls/Program Finance

IBR support

Deltek Cobra implementation and system administration

Position your programs for stronger performance transparency and executive confidence. Unlock The Alchemy of EVMS Excellence™ with Elixir Value Management Systems.

EVMS · Project Controls · Deltek Cobra

📧 karlo.menoscal@elixirvms.com

📞 949-351-8896